Interest Rate Cap Floor Straddle

:max_bytes(150000):strip_icc()/understandingstraddles2-c0215924b5ba43189e1a136abc5484bf.png)

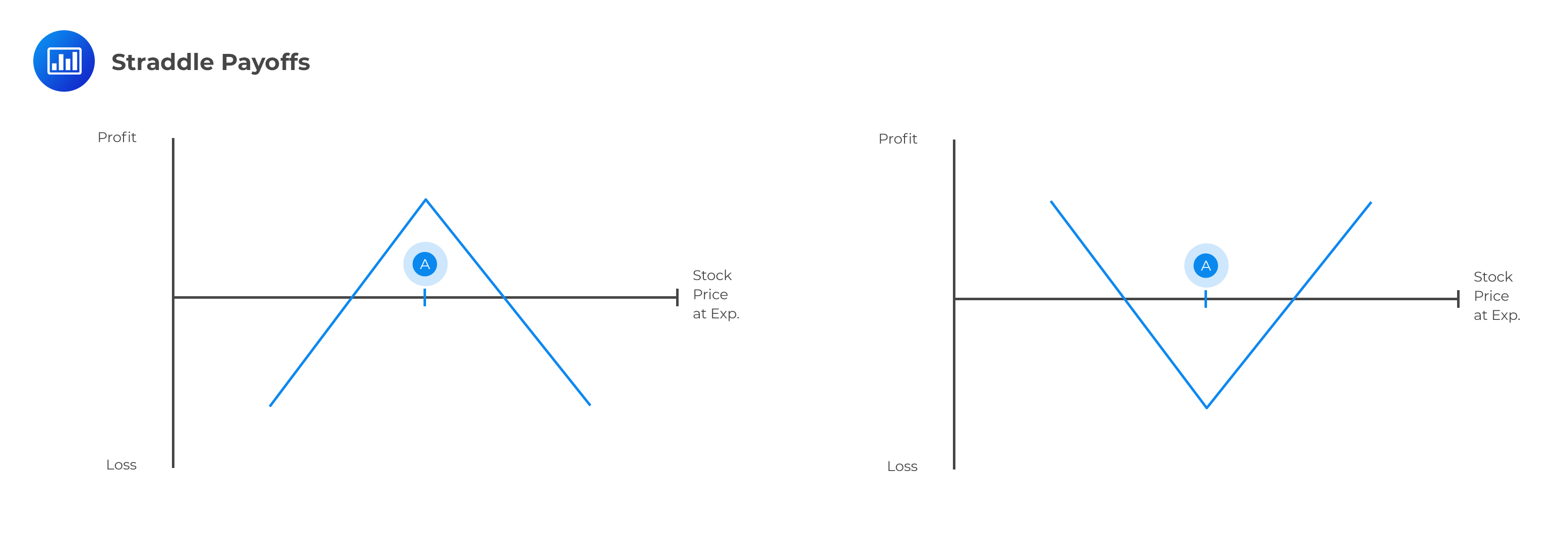

Straddle Definition

Trading Strategies Involving Options Analystprep Frm Part 1

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

10 Options Strategies To Know Put Option Interactive Brokers Writing Strategies

7 Popular Options Trading Strategies Magnifymoney

Long Call Ladder Explained Online Option Trading Guide

Time 0 5 6 004 0 470 4 721 0 021 35 0 06004 0 04721 0 470 0 021 ir modeling a capped floater consider an investor holding a 2 year.

Interest rate cap floor straddle.

Long Straddle Definition Day Trading Terminology Warrior Trading

/10OptionsStrategiesToKnow-02_2-8c2ed26c672f48daaea4185edd149332.png)

Protective Put Definition

Managing Risk Via The Financial Markets In The Uk Financial System Fifth Edition

Installation Instructions Installation Instruction Installation Instructions

Source : pinterest.com